Happy New Year! We hope you had a joyful holiday season and wish you a healthy and prosperous 2020!

The U.S. stock market returned sizable gains for 2019, with the S&P 500 appreciating 28 percent. This was quite a turnaround from late 2018 when the S&P 500 declined by 19 percent, reaching an oversold reading, ending the year with a 6 percent loss. But a lot had changed over the course of the year, and the concerns and fears of 2018 (U.S./China Trade war, The Federal Reserve raising rates, global slowdown) reversed course in 2019, providing a productive backdrop, most notably the Fed reversing its course of interest rate increases and providing a series of interest rate cuts during the year. This reversal in rate regime put a floor under the market and helped it march higher and achieve a series of new all-time highs in 2019.

Not to say there were no risks or worries in 2019, quite the contrary. While trade tensions had eased somewhat, there was still concern about the volatile political climate and whether the trade agreements would actually be implemented. The splitting of one large grand deal into several phases left a concern of ongoing spats and potential future “no deals”. Also, in the middle of the year, corporate earnings began to notably decline, the yield curve inverted, and trade agreement concerns re-emerged, leading to an uptick in volatility which resulted in a 7 percent drawdown in May and August, and a 5 percent drawdown in September. At a similar juncture, we observed a fractured undecisive market, where growth and momentum sold off hard and value and defensive sectors shot higher, only adding to the confusion. Finally, the prospects of the market being too exuberant, complacent, and having gone too far too fast concerned a lot of market observers, predicting a blow off top and a subsequent reversion to the mean may be lurking around the corner.

All of the good and bad led to a lot of confusion and uncertainty of market direction. The market ended the year on a high note, shrugging off the earnings deceleration and continuing to attract new dollars, pushing the indices higher into year end.

We spend a lot of time working with each of you to determine your acceptable range of risk, returns and volatility that are appropriate for your tolerance. We focus on standard deviation, the industry measuring tool of volatility and risk, to help us design durable portfolios that will help you stay the course under various market environments and better insulate you from sizable losses while simultaneously enabling you to participate in your fair, risk appropriate share of market advances. While standard deviation matters less when the market is going up, it is imperative that we continue to be mindful of the other side of the equation, in advance.

So what is standard deviation (“SD”), and why does it matter in portfolio construction?

“Standard deviation is a statistical measurement in finance that, when applied to the annual rate of return of an investment, sheds light on the historical volatility of that investment. The greater the standard deviation of securities, the greater the variance between each price and the mean, which shows a larger price range” https://www.investopedia.com/terms/s/standarddeviation.asp

Bear with us as we expound with more statistical verbiage. SD is the variance around the average or deviance from the expected behavior of a particular investment. The higher the SD the greater variance, or deviance, the movement of an investment from what is otherwise historically experienced from its average (mean) behavior. A SD lower than its benchmark should thereby reduce the drawdown of a portfolio during market declines. One of TWG’s philosophies of portfolio management is managing risk, partly by reducing full participation in sustained market declines that are ultimately more detrimental in your ability to meet your investment objectives than full upside capture. This concept can be understood by simple math. A 50 percent loss requires a subsequent 100 percent gain to get back to where it started ($100 – $50 = $50 + $50 = $100). A 25 percent loss requires a subsequent 33 percent gain ($100 – $25 = $75 + $25 = $100). The severity of a loss has a greater impact than the magnitude of a gain. The challenge then becomes one of optimizing a portfolio to respond favorably (on a relative basis) in both good and bad market environments, ideally capturing a higher percentage of the market upside and less of the market’s downside (upside/downside ratio) over time.

To accomplish this (because we do not attempt to predict the direction of the market) we focus on standard deviation and utilize a rules-based process to proactively reduce or increase risk exposure. As the market declined in the final months of 2018, our process systematically reduced risk exposure, accumulating cash in your accounts as the market declined. We entered 2019 with a healthy cash position from following our rules, which would have insulated you from further market declines should they have continued. However, as the market bottomed in late December 2018 and began to rebound, our process systematically re-positioned the accumulated cash back into risk assets to participate in further potential market advances. We were back to being fully invested to our target allocation by the end of February and remained fully invested for the balance of the year.

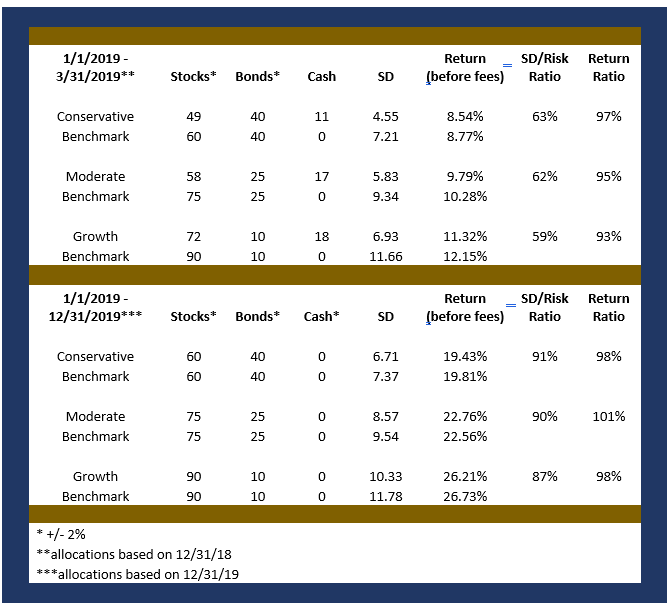

On the following page is a matrix of the allocations, SD, returns (after fees) and risk/return ratios for actual accounts that represents each of our model portfolios, compared to its benchmark^, that resulted during two periods in 2019 – the first quarter and full year. Note the cash position as of 12/31/2018 as we entered 2019.

You can compare the difference in SD during the 1/1 to 3/31/2019 reporting period after we had proactively accumulated cash during the 4Q2018 market decline and the corresponding risk/return ratios. After the 4Q2018 downtrend the 1/1 to 3/31/19 portfolio SD was much lower relative to the benchmark SD than it was during the 1/1 to 12/31/2019 report period when the market was in a confirmed uptrend. Performance was in line (before fees) with the benchmark but did so with less risk (lower SD) to balance risk and return. We quickly re-invested the cash over the course of January and February 2019 and were thereafter fully invested to our target allocation for the rest of the year. You can also observe the difference in SD during the full year 1/1 to 12/31, performing in line (before fees) with the benchmark but again doing so with less risk (lower SD), and also fully invested. It is the risk adjusted return that ultimately becomes paramount during sustained market declines.

We hope this Market Pulse provides greater understanding of our rules-based process of seeking out returns in rising markets while simultaneously managing risk in declining markets. In our opinion, the returns speak for themselves, and we look forward to continuing to help you achieve your financial goals and objectives and proactively managing your investment accounts in a prudent manner.

Because the information on this blog are based on my personal opinions and experience, it should not be considered professional financial investment advice. No financial decisions should be made based off this article without consulting with your financial advisor first.