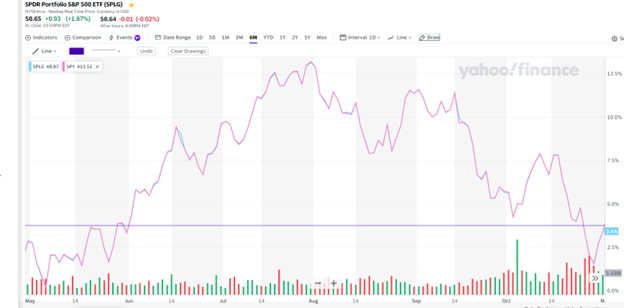

The market started the month moving higher but rolled over mid-month to mark the third consecutive down month. The S&P declined 2.1%, the NASDAQ slipped 2.78%, S&P equal weight shed 4.18% and small caps dropped 6.88%. Bonds lost 1.8% as rates neared cycle peaks, clearly putting pressure on equity valuations.

QQQ, our largest position, declined 2.08%, and COWZ lost 2.8%. The rest of the developed works (CWI) declined 3.2%

Energy was the worst performing sector, down 6%. Utilities gained 1.3%, but are still the worst sector YTD, down 13.3%.

TWG Moderate and Conservative declined less than their respective benchmark after 3Q fees, while TWG Growth slightly underperformed its benchmark after fees.

NOVEMBER SNEAK PEAK – as we were finishing this note, we wanted to add in some positive developments. For the week starting 10/30 the S&P rallied 5.88% – its best week of the year. This rally recovers all the losses from October and the second half of September and reclaims the 50-day moving average.

WHAT MOVED THE MARKETS

Ten year treasury yields continued their ascent towards 5%, putting additional pressure on valuations, particularly growth assets.

Strong economic data continues to point to resiliency of the U.S. economy. Retail sales came in hotter than expected, suggesting the consumer continues to spend. Another data point indicated that pandemic-related savings rates are higher than previously estimated, thus keeping additional fire power for the consumer to continue to spend. Jobless claims dipped, implying companies are not laying off as many employees as one would expect given the macro backdrop of higher rates.

All of this “good” news may keep inflation elevated, and perhaps slowed down its descent to the Fed’s favored 2% range. Powell’s speech to the economic club on 10/19 reiterated the likelihood that rates will need to stay “higher for longer” so long as the economic data continues to come in stronger than expected. If said strong growth leads to resurging inflation, additional tightening might even be required. Another talking point that rattled markets was that economic conditions may not be tight enough, suggesting that the Fed may have to raise rates even more, even though, theoretically, the bond market is doing some of the Fed’s work as rates are moving higher than the Fed funds rates pace of change. This speech seemed to be what caused the market to roll over for the balance of the month.

The path of recovery has become more uncertain given the tug of war between strong economic readings and the Fed’s signaling of future path of higher for longer.

To better understand the impact of rising rates, in August the 10-year treasury rate was around 4% and pierced 5% towards the end of October. A 25% increase in yields over three months is clearly pressuring stock prices.

At the end of month GDP for 3Q was released, showing the economy grew at a faster pace than expected – 4.9%. This was almost double the rate during the 2Q and indicates a strong and growing economy. However, GDP is a backward-looking indicator, and with such strong data, the market is again questioning whether the Fed will have to raise rates more, or if the higher yields in the bond market are taking care of that for them. This is yet another sign of good news is bad news, as a strong economy theoretically challenges the narrative that inflation will continue to decline towards the Fed’s 2% target which would enable them to consider cutting rates down the road.

The bull/bear tug of war can be summed up in a few ways. For the bull case- the economy is strong – reflected in part by higher long-term rates. Jobs are plentiful, which supports ongoing consumption. Investor sentiment has declined over the past few months and average equity exposure is much lower than positioning over the summer. This can set the stage for a year-end rally with higher odds than if the market was elevated and everyone was optimistic of a year-end rally.

Now the Bear case – there are signs of an economic slowdown; student loan repayments tap some cash flow that would otherwise be spent on goods and services, and the summer “revenge” travel is largely in the rear view mirror. Credit delinquencies are trending higher, particularly in the bottom half of income earners, and if rates stay elevated for an extended period of time, additional cracks will likely form.

3Q EARNINGS

Earnings have generally come in stronger than expected, but the market reaction to said earnings have generally been weak. Those companies that reported lower than consensus got taken to the woodshed, and companies that beat, often handily, often too got punished. Take Alphabet and Meta, who both posted earnings, top and bottom-line revenue growth well in excess of expectations. They sold off. Alphabet sold off 10% the day after their strong earnings, and Meta fell close to 5%. Forward guidance has been key, and generally the guidance provided by companies reporting earnings has been one of concern and uncertainty.

If the earnings trend continues to show growth, then the prior three quarters of negative earnings could be behind us. A trough in earnings decline historically sets the stage for future gains, as earnings growth accelerates out of an earnings recession and is supportive of higher future valuations.

We believe that the market is looking forward (as it usually does) and is extrapolating that 3Q earnings may be as good as they’re going to get for a while, given the uncertainty of future economic strength. Perhaps it’s also that these mega cap tech names have already run up significantly ahead of 3Q earnings, so any weak future guidance becomes a cause for concern, and a reason to take profit. Another way to look at this “sell the news” type of market is that the froth is being taken out of the market, which could set it up for larger gains in the future. Valuations were stretched coming into earnings season, and, after these selloffs, are much less stretched. Forward 12-month Price/earnings for the S&P 500 is 18, below the five- and 10-year averages. This valuation metric can set the stage for more productive future advances at a time when there is a bit more clarity around the economic impact of rates, and the higher for longer mantra becomes a bit clearer as to how much higher and how much longer.

Fifty-six percent of S&P companies have reported Q3 earnings, and 80% have reported a positive EPS surprise. Average EPS beat is 7.8%.

PORTFOLIO ADJUSTMENTS

The market has moved sideways for about five months, and at the month’s end the S&P closed at levels last visited in mid-May.

Over the past couple of months in particular, the trends have been very brief and abrupt. Most of the trading activity has been shifting from QQQ’s to COWZ, and S&P to GCOW. A bit of back and forth, and emblematic of a trendless market. However, once a trend becomes more persistent, we should be well positioned to ride said trend higher. Until such stability, we’ll continue to jockey for positions that are trending in the right direction, regardless of how short these trends may last.

LOOKING AHEAD

We recognize that a sideways market is frustrating and a bit unsettling. With markets declining double digits in 2022, a surprise rally to start 2023, and the recent three straight months of declines, on the surface it seems like it may be better to move to the sidelines and wait for this volatility to disappear. This is rarely a viable investment strategy, evident by the sharp rebound in January 2023 and again last week. Widening the view, at the end of October the S&P 500 is trading at levels going all the way back to May 2021 – a full 30 months of going nowhere with a lot of ups and downs in between. However, it is not unusual for the market to trend sideways (consolidate) during periods of dramatic change. This time, a normalization of rates is the culprit after 10+ years of below average interest rates. It will take some time for the markets to settle into this dramatic shift, but the economy typically emerges stronger after a period of discomfort. We will get through this challenging time and eventually welcome a period of greater, more consistent productivity.

With the bounce we saw at the end of October that carried into the first week of November, we remain optimistic that a year-end rally can continue. However, we are aware of the signs of economic activity beginning to cool off. Most of the data over the past several weeks are pointing to a slowdown – in spending, hiring, wage growth, supported by corporate America’s cautious forward guidance. The full effects of the Fed’s rate increases have yet to be fully absorbed, and the long and variable lags of monetary policy will continue to impact future economic activity. The fed last raised rates during its July policy meeting, and we welcome and appreciate their willingness to take pause to see how things play out.

On the one hand, a strong economy not only delays a technical recession (if there is one), but it also challenges inflation continuing to decline. Without inflation moving closer towards the Fed’s 2% target, the Fed will be hard pressed to cut rates in the near future. However, as ongoing data continues to point to a slowdown in economic activity, demand should begin to wane, which will be positive for inflation continuing to come down. How cool the economy gets is still to be determined. While the soft-landing narrative is still on the table, it is very difficult to slow down the economy to quell demand and reduce inflation in the absence of a recession. From our point of view, there is still a probability that the economy will still slow down and bring with it a mild recession. Even a mild recession can get inflation back to the Fed’s target, at which time they should be more comfortable starting to reduce rates, which should lend to an increase in economic activity and enable the economy to begin to grow again post-recession.

For now, we take comfort in the strong 3Q GDP, and feel that if there is a recession, it is still several quarters ahead, and not imminent. Energy has pulled back, which is another welcome relief for a big inflationary force.

We remain optimistic that the balance of the year is supportive of higher equity prices and will continue to ride the trend higher should it be maintained. As of 11/6 we are again positive YTD and remain confident that our strategy will assist in our seeking out exposure to areas of the market that are trending higher and reduce or eliminate areas of the market exhibiting weak price movement.

We wish you a Happy Thanksgiving with family, friends and a lot of food and laughter. Please remember to be grateful for all of the blessings we have in our lives.