March 2024 and a 12-month Recap

The stock market continued its advance to close the month quarter. For March, the S&P gained around 3%, the DJIA advancing around 2% and the NASDAQ was the underperformer of the major indices with gains around .7%. S&P 500 equal weight advanced 3%. Mid-caps and small caps gained 5.4% and 3% respectively. Value (RPV) soared around 5.5% while growth RPG gained 1.2%. The rest of the developed world advanced around 2% and bonds shed .75%.

TWG growth, moderate and conservative portfolios all extended their year to date performance with gains around 2.45%, 2.2% and 1.9% respectively, slightly lagging their respective benchmarks.

For the quarter, TWG growth, moderate and conservative portfolios advanced around 7%, 6% and 5% respectively.

WHAT MOVED MARKETS

Fed speak and bond yields once again led the market moves.

On March 12, February inflation data came in hotter than expected, creating a potential trend of inflation no longer falling month after month as the drop stalled in January. Now we are seeing two months of small month over month increases in CPI. Headline inflation ticked up to 3.2% and core inflation (excluding energy and food) ticked down to 3.8% from 3.9%. While the two metrics moved in opposite directions, said move does not support declining inflation. Nor does it signal caution that inflation is ramping higher. The market took the data in stride, however, and rallied to new highs.

Once again, the categories that accelerated at a pace greater than the 3.2% inflation rate were auto insurance, rent, restaurants and housing, as has been the case for some time. Other categories are seeing price declines, such as rental cars, airfare, used vehicles and some goods categories like toys, appliances and furniture.

Producer price index data rolled in the next day, confirming a tick higher in prices given by CPI the day prior.

As the month and year’s rise in inflation is far from a spike, even if inflation stays flat for a few months, it’s better than a re-acceleration in prices. However, with two months of small price increases, the data would imply that the timing of the first Fed rate hike gets pushed out farther into the year.

The Federal Reserve meeting on March 20th was an important one considering the previously mentioned hot inflation data. Investors were worried that the Fed would signal concern about its fight against inflation and wondered whether the Fed would keep rates higher for even longer. Remember, at the start of the year, the market was pricing in the first rate cut in March, and here we are. Expectations have changed quite a bit over the past months, but the data reflecting a tick up in inflation had investors on edge.

The Fed soothed this concern, and expressed confidence that inflation will still continue to moderate, notwithstanding recent, and expectant, lumpiness. The Fed also hinted that cuts are still the most likely next move and sticking to their previously mentioned three cuts in 2024. Markets spiked higher on the heels of Powell’s presser, closing the day up over 1% and at new all-time highs for all three indices.

Bond yields, however, backed up, with the yield on the 10-year U.S. treasury spiking from around 4% early March to 4.3% in the middle of the month. Yields rolled over in the following week but as the month ended, yields were once again knocking on the 4.3% level. This volatility in rates impacted equity movements. It’s not that the stock market can’t support a 4% rate environment, but the rate of change in yields creates uncertainty that bleeds into market sentiment, as market participants try to gain clues as to when, and how much, the Fed may cut rates this year (if at all).

PORTFOLIO ADJUSTMENTS

As mega cap tech started to show signs of exhaustion that translated into lagging the broad market, we pragmatically reduced exposure to our largest position – QQQ- which is our preferred large cap growth fund. Proceeds were repositioned to some international exposure and value.

To start the month, we were overweight in large growth. At the end of the month, we had a nice core position in the S&P 500, and almost an equal weighting of growth and value. As the market appears to continue its broadening out, our positioning reflected the same as we balanced growth and value as the tug of war between rates and growth and value ensued.

ONE YEAR IN REVIEW

It has been a full year since we implemented our 50-model strategy and the improvements have been notable. Over the course of the past 12 months, the market started with extremely narrow participation, mostly the “magnificent seven” mega cap tech stocks providing the majority of the market gains during the first three quarters of 2023. Fall of 2023 ushered in a 10% pullback and heightened volatility. From November 2023 through March 2024, market participation broadened out significantly, implying less dependence on the market gaining solely on the shoulders of the largest tech stocks in the U.S.

Case in point. So far in 2024, the “magnificent 7” has morphed to the “fabulous 4”. Only Nvidia, Meta, Amazon and Microsoft have outpaced the broad market. Google slightly underperformed, Apple declined 10% and Tesla cratered 30% so far in 2024.

We welcome an environment where more than a handful of companies are carrying the market, which in our opinion are signs of a healthy economy.

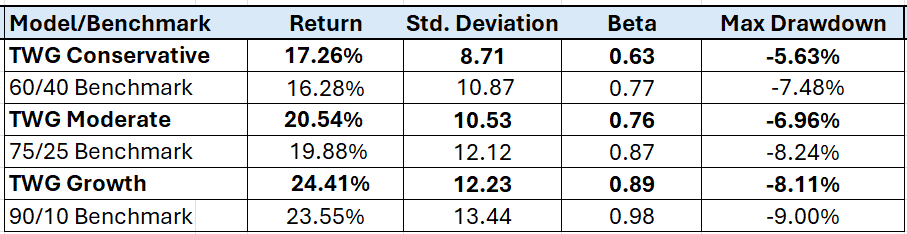

We’ve compiled statistics for the TWG model portfolios to demonstrate the effectiveness of our trading strategy. Our objective is to deliver superior risk adjusted returns within a specific risk mandate. Stated differently, over a full market cycle we strive to provide returns greater than their benchmark while taking less risk.

The following statistics are for the period from 4/1/2023 to 3/31/2024, before fees:

The statistics show that our goal has been achieved over the past 12 months in a generally rising market. This period did not require all that much risk mitigation, as the market emerged from steep declines in 2022 and entered a new “bull” market. When the market is moving up and to the right, we strive to capture our fair, risk-appropriate share of market gains. However, when the market is moving down and to the right, our process of moving to less risky investments and even raising cash, should offer downside protection. It is over a full market cycle, if we do not fully participate in market declines yet participate in market advances to a great extent that our strategy is expected to outperform its benchmark, thus creating value.

LOOKING AHEAD

As the market has surged over 20% from the October 2023 lows, we find that parts of the market are overextended. We could envision hitting a pocket of less productivity as the market digests recent gains. A period of sideways consolidation is more likely, in our opinion, though a modest (5-7%) pullback is not out of the question.

We think that a moderation in the pace of near-term gains is healthy and sets up for higher highs later in the year. Of course, the upcoming earnings season will likely determine the upcoming quarter’s trajectory.

Inflation will continue to be an important data point to watch, as we believe some of this year’s gains are predicated on multiple rate cuts this year. But cuts are not a forgone conclusion, particularly if inflation continues to come in hotter than expected or only moderates slightly.

But we take solace in the fact that most data points to a strong economic backdrop – low(er) inflation, low unemployment, moderate wage growth, moderating inflation and increasing corporate earnings. All of this in a 5% rate environment is something that most economists probably didn’t believe possible just one year ago.

While we don’t know what the immediate future of market productivity will bring, we do know that our strategy is very flexible and will respond to any dramatic changes beneath the surface.

Enjoy the early days of Spring! Until next month!